Wellness Economy Statistics & Facts

The Global Wellness Institute (GWI) is recognized as the leading source for authoritative wellness industry research. Since 2007, the GWI has commissioned and published numerous research reports on the global wellness economy, including our flagship publication, the Global Wellness Economy Monitor. All reports are available free to the public. Data highlights from recent studies are below. To download all GWI research, including special reports for certain industry sectors and geographic areas, visit Wellness Economy Research.

Global Wellness Economy

GWI is the first and only organization to conduct comprehensive, objective, and global research on the wellness industry. We first defined and measured the wellness economy and its component sectors in 2014, these figures are now updated and released every year in the Global Wellness Economy Monitor. Our most recent report, Global Wellness Economy Monitor 2025 (released in November 2025), provides data for 2019-2024.

The Global Wellness Economy in 2024

AT A GLANCE

-

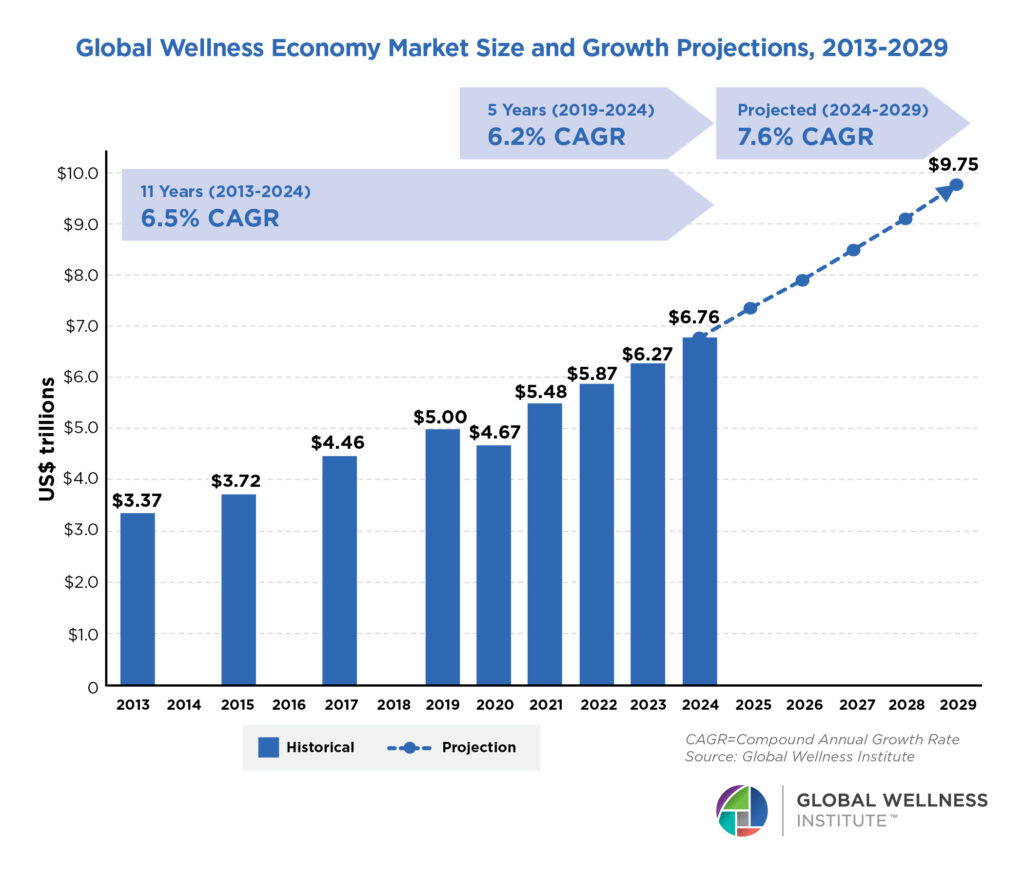

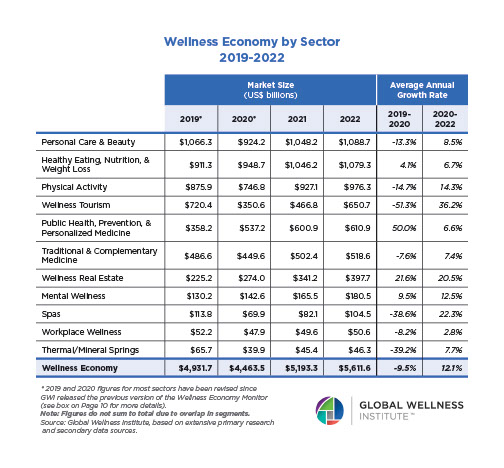

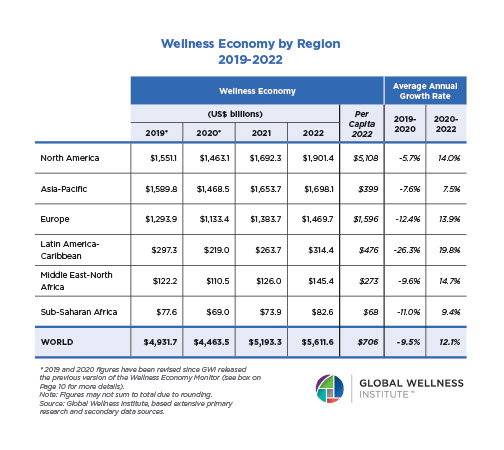

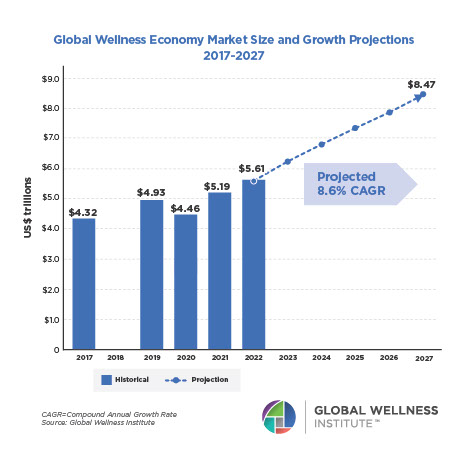

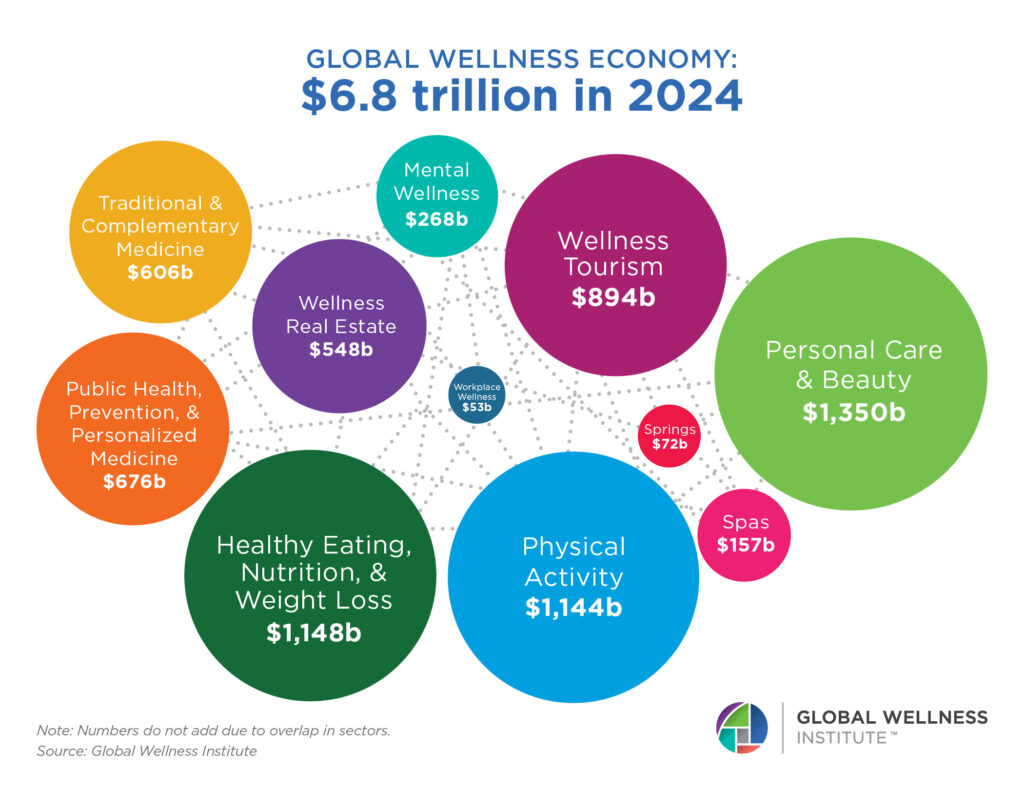

- The global wellness economy grew by 7.9% from 2023-2024 and reached a new peak of $6.8 trillion in 2024. It has doubled in size since 2013.

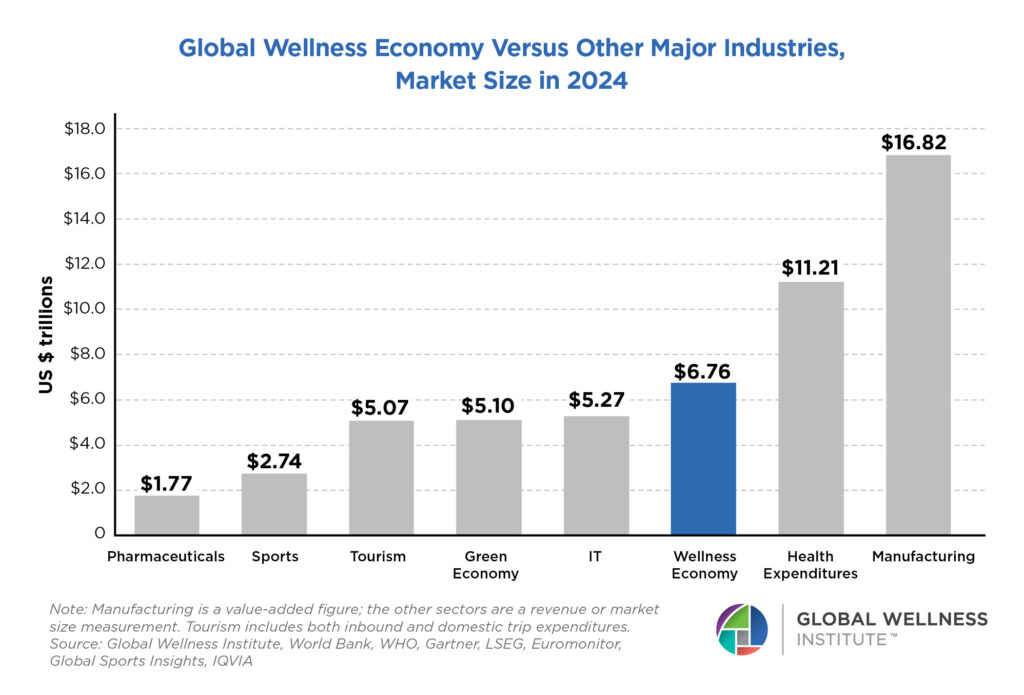

- The wellness economy is a major force in the global economy, larger in size than the green economy, IT, tourism, and sports.

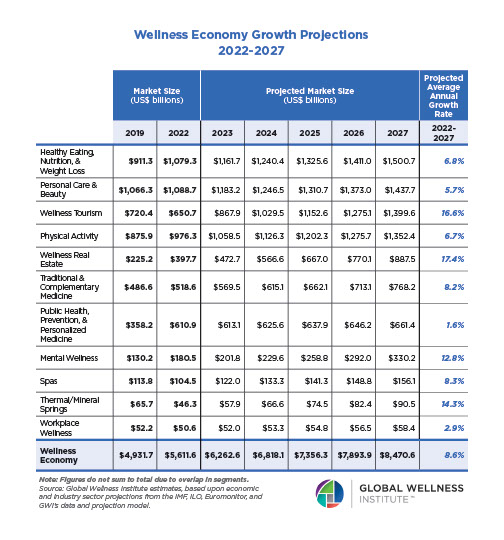

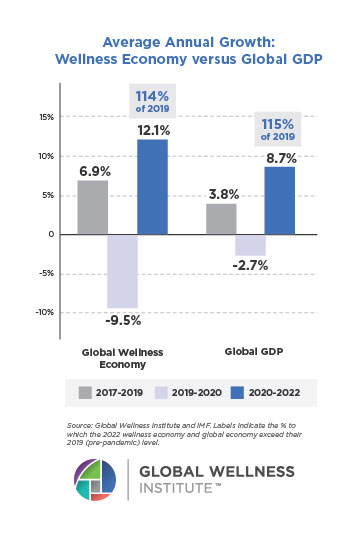

- The global wellness economy has consistently grown faster than the global economy. Looking over the long term, wellness grew by 6.5% annually from 2013-2024, while global GDP grew by 3.2% annually. Wellness represents 6.12% of global GDP as of 2024.

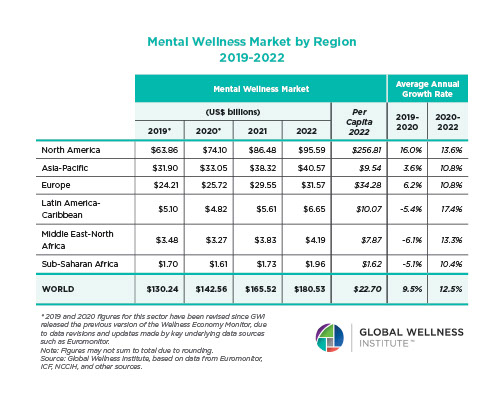

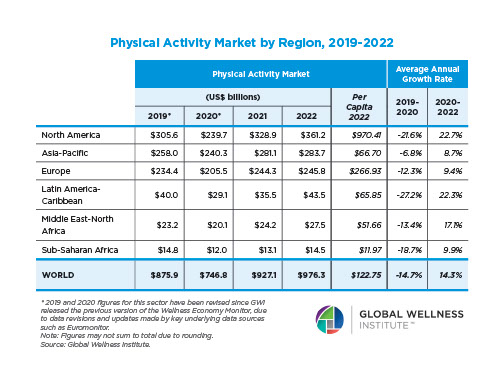

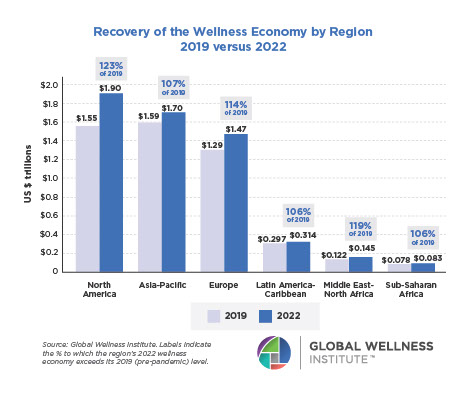

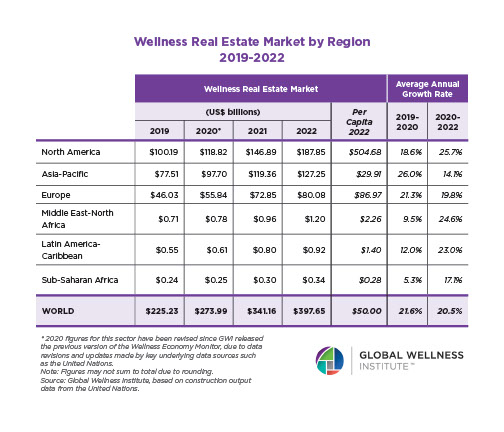

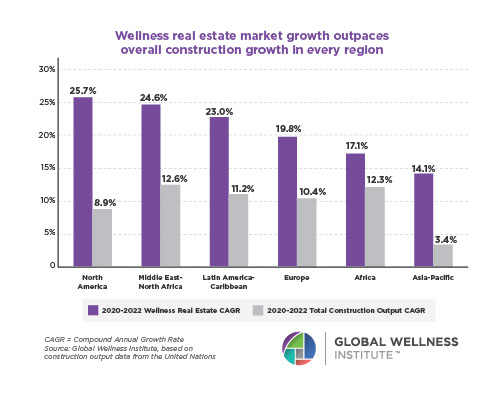

- North America, Middle East-North Africa, and Europe are the fastest-growing regional wellness economies over the last five years and have shown the strongest resilience and recovery in the post-pandemic period.

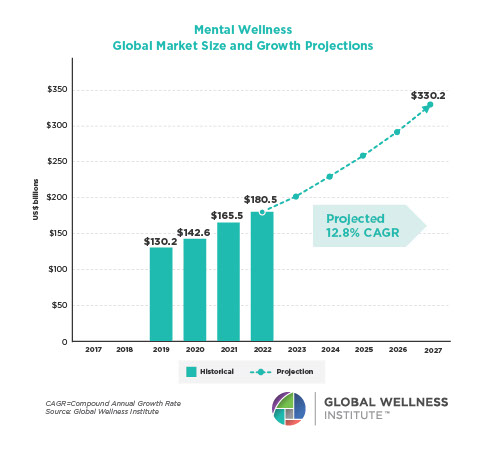

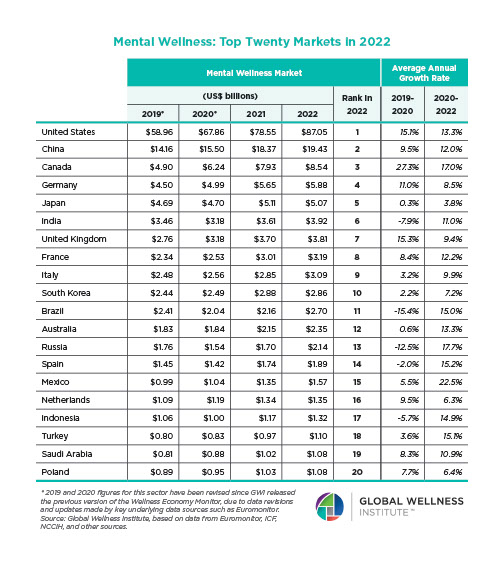

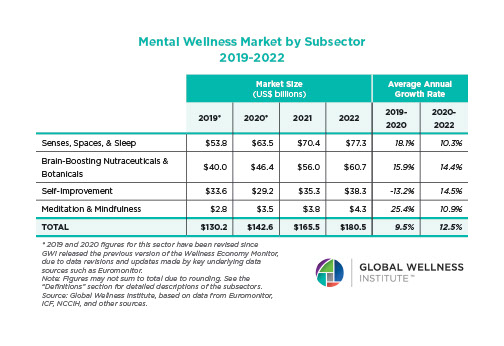

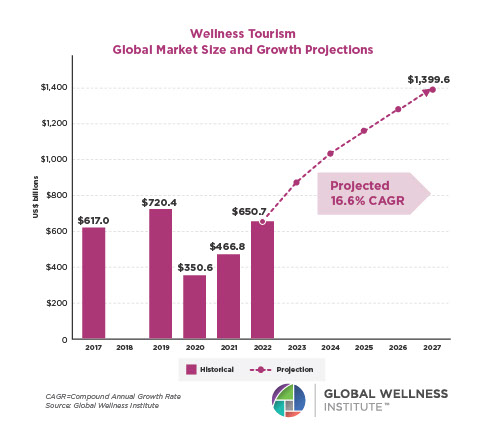

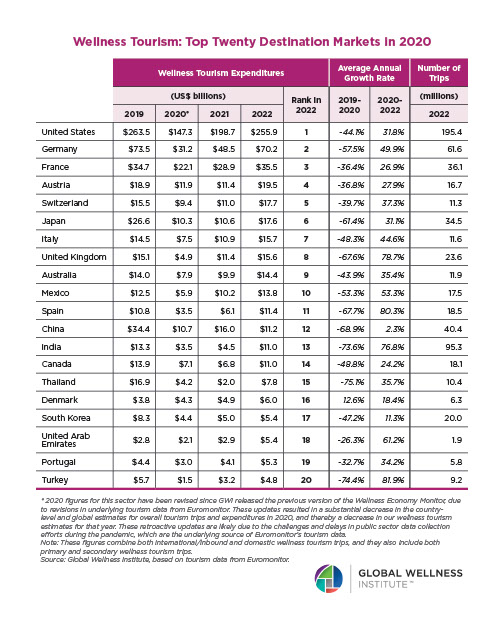

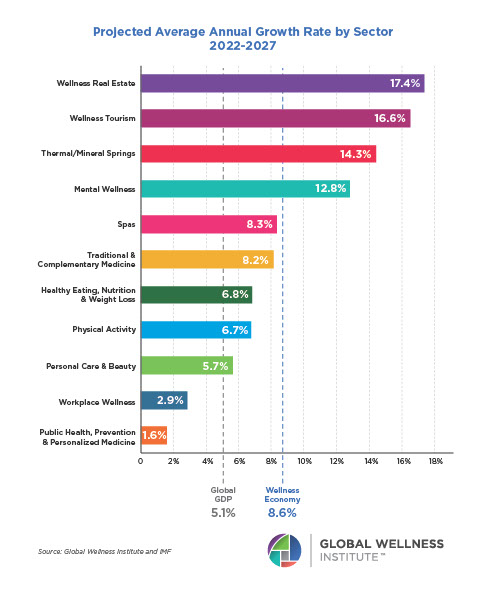

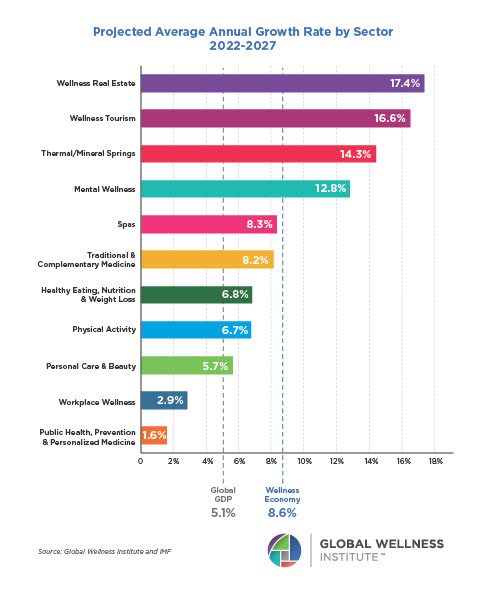

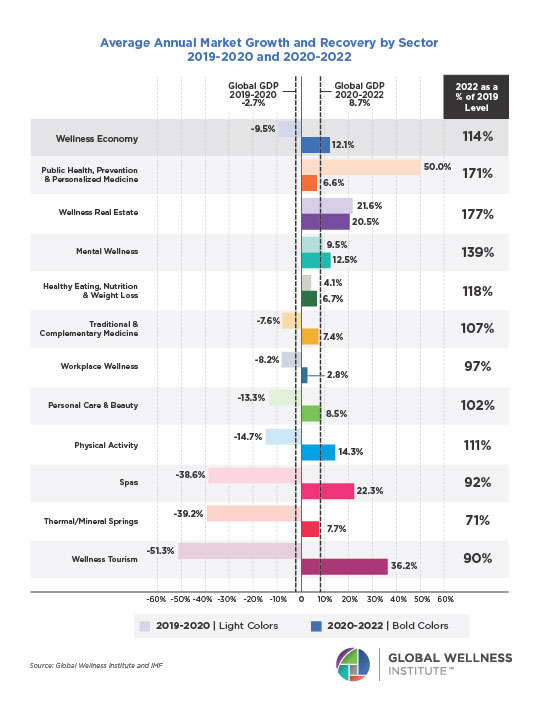

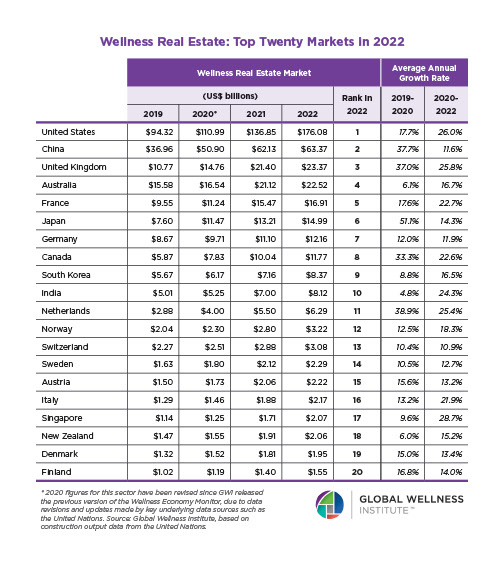

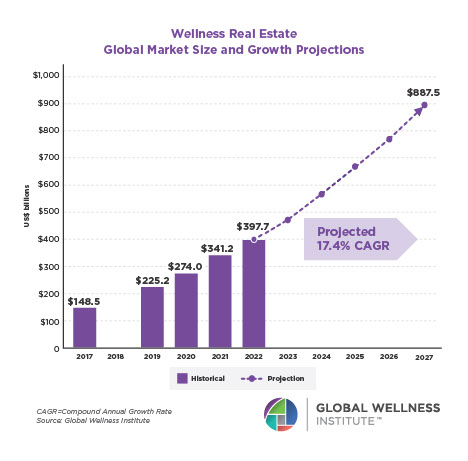

- All of the eleven wellness sectors have fully recovered from the pandemic, with a 2024 market size that exceeds their 2019 level. Wellness real estate and mental wellness are by far the fastest-growing sectors, expanding at average annual rates of 19.5% and 12.4%, respectively, from 2019-2024.

- We project the global wellness economy will expand by 7.6% annually from 2024-2029, a growth rate substantially higher than the projected global GDP growth of 4.5% (according to current IMF forecasts). The wellness economy is expected to reach nearly $9.8 trillion in 2029.